Labor Cost Calculator + How To Use It

Use the labor cost calculator to get an accurate estimate for informed budgeting or pricing decisions.

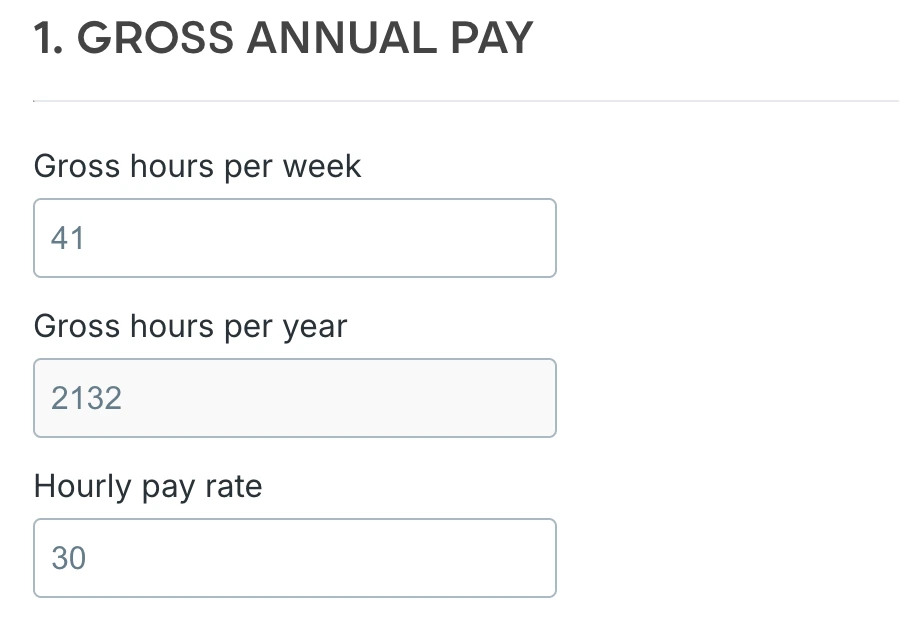

1. GROSS ANNUAL PAY

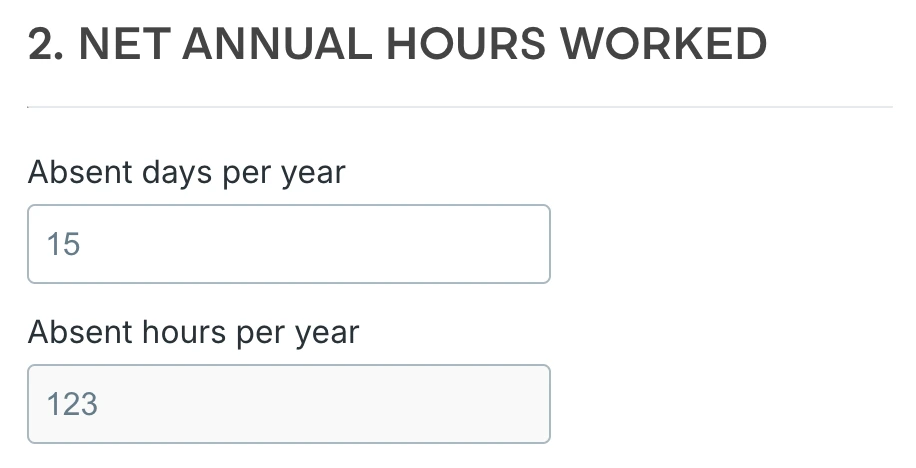

2. NET ANNUAL HOURS WORKED

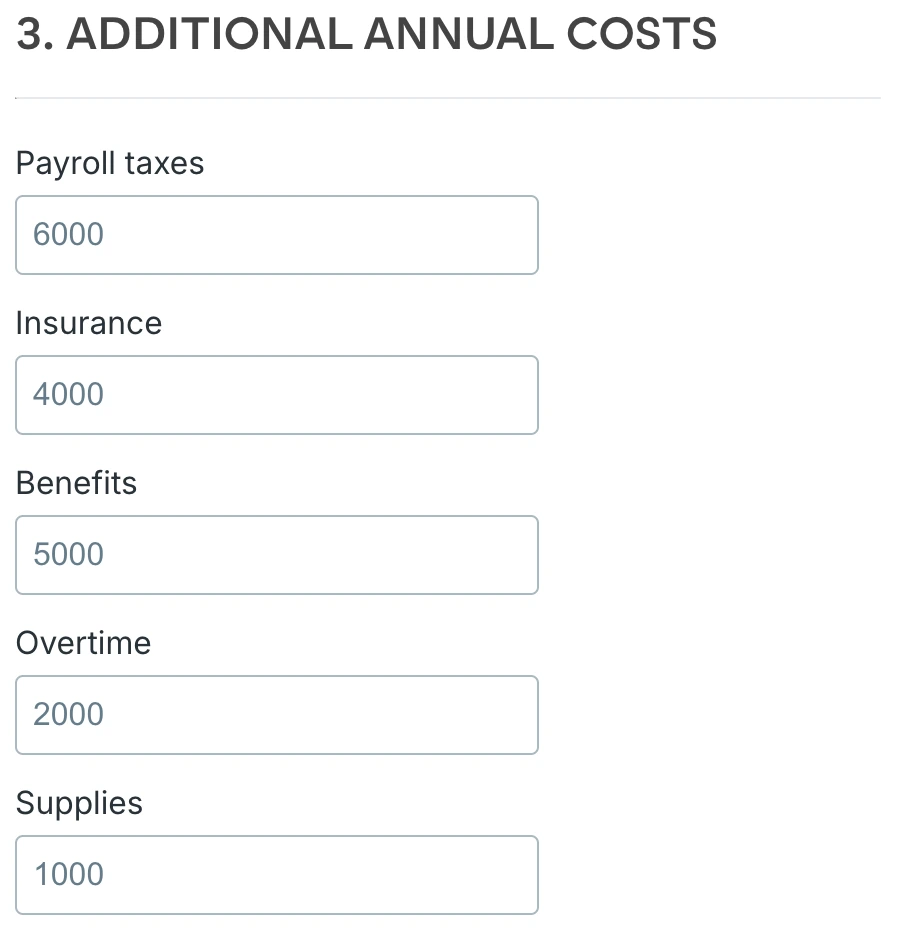

3. ADDITIONAL ANNUAL COSTS

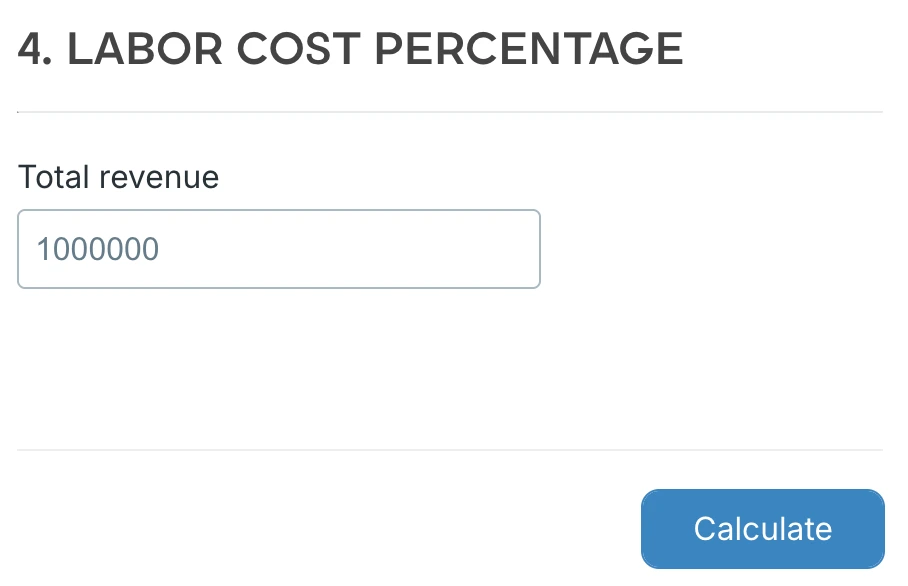

4. LABOR COST PERCENTAGE

What are labor costs?

Labor costs are the total amount a business spends on its workforce. Besides base wages, labor costs include the following expenses:

- Overtime pay,

- Bonuses,

- Payroll taxes,

- Health insurance,

- Retirement contributions,

- PTO, and

- Other company-provided benefits such as meals, phones, or vehicles.

Calculating labor costs accurately helps you make confident budgeting and pricing decisions, which is essential for your business success.

Labor costs are divided into 2 categories:

- Direct, and

- Indirect labor costs.

Learn more about each category below.

Direct vs indirect labor costs

Direct labor costs are expenses for employees who directly deliver services or produce goods for a business. Examples of direct labor costs are:

- Wages of assembly line workers in a factory,

- Pay for construction workers building a structure, or

- Wages of cooks preparing food in a restaurant.

Indirect labor costs are expenses for employees who support production but aren’t directly involved in making a specific product. Common examples include the wages of supervisors or administrative personnel.

Understanding how indirect labor costs, like wages of supervisors or administrative staff, support your business can help you feel better equipped to manage overhead effectively.

What’s a labor cost calculator?

A labor cost calculator is a tool that helps employers determine the true cost of labor, including employee wages, payroll taxes, and benefits. This tool simplifies estimating your labor costs, making it easier to avoid undercharging and feel more in control of your profit margins.

How our labor cost calculator works

Our labor cost calculator has 4 sections. To determine your annual labor cost per employee, fill out these sections one by one.

Section #1: Gross annual pay

Enter the total number of hours worked by an employee in a week (including overtime) in the Gross hours per week field (e.g., 41). After you provide this information, your employee’s gross hours per year (in this case, 2,132) will appear in the Gross hours per year field.

Next, enter the amount of money paid to that employee per hour in the Hourly pay rate field (e.g., $30).

Section #2: Net annual hours worked

Net annual hours worked represent the total number of hours an employee actually works in a year, excluding PTO and any other non-work time. They’re computed by subtracting annual absent hours from annual gross hours.

Enter the total number of their absent days per year (e.g., 15) in the Absent days per year field. As soon as you provide this information, your employee’s absent hours per year (in this case, 123) will appear in the Absent hours per year field.

NOTE: An employee’s absent days represent the total number of days an employee is absent from work due to illness or vacation.

🎓 What Is Absenteeism? Causes and Consequences

Section #3: Additional annual costs

Enter the amounts of money you pay per year for other employee-related expenses, including:

- Payroll taxes (e.g., $6,000),

- Insurance (e.g., $4,000),

- Benefits (e.g., $5,000),

- Overtime (e.g., $2,000), and

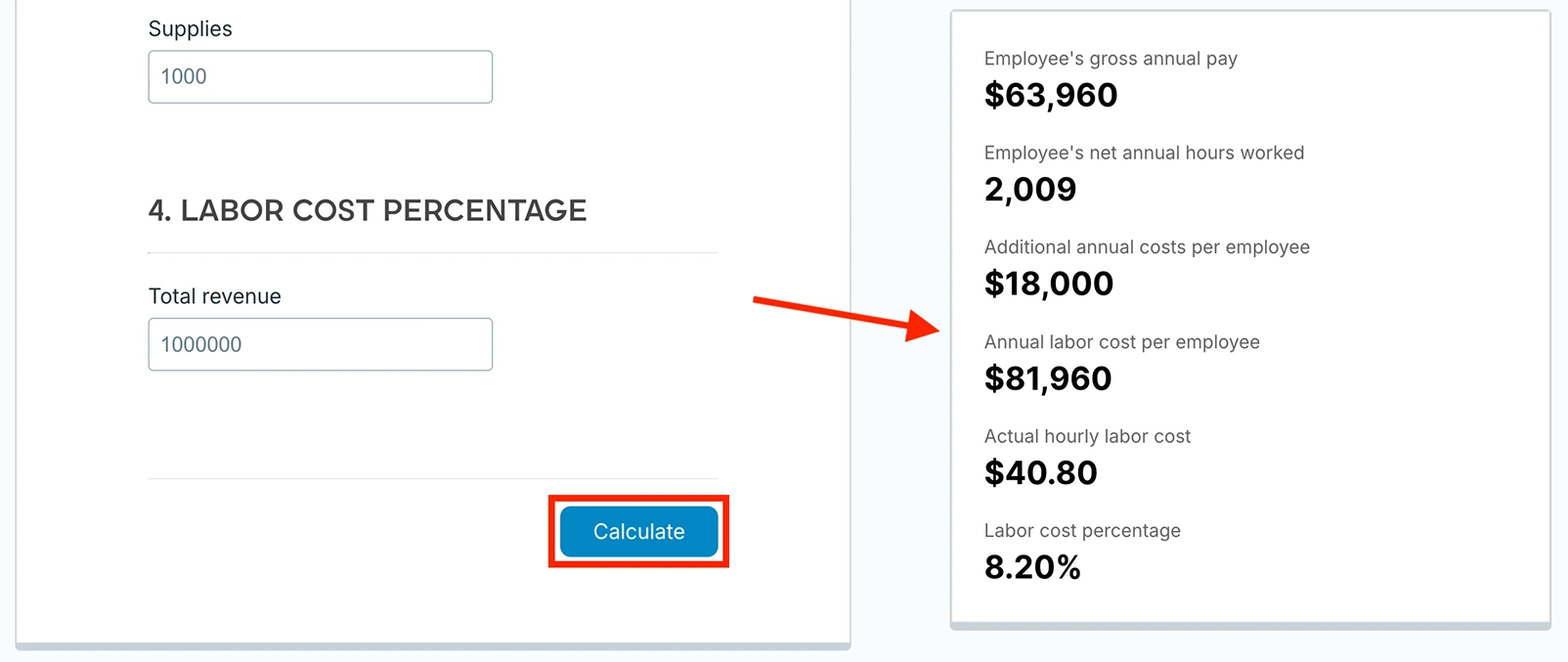

- Supplies (e.g., $1,000) in the appropriate fields.

Section #4: Labor cost percentage

Enter the total revenue generated by your company in a year (e.g., $1,000,000) in the Total revenue field.

When you fill out the sections and click Calculate, you’ll see your:

- Employee’s gross annual pay (in this case, $63,960),

- Employee’s net annual hours worked (in this case, 2,009),

- Additional annual costs per employee(in this case, $18,000),

- Annual labor cost per employee (the sum of your employee’s gross annual pay and additional annual costs — in this case, that’s $81,960),

- Actual hourly labor cost (in this case, $40.80), and

- Labor cost percentage (in this case, 8.20%) under the appropriate titles.

What are the steps to calculate labor costs?

To manually calculate your annual labor cost per employee, follow the 6 steps explained below.

Step #1: Determine the gross pay per employee per year

To determine your employee’s annual gross pay, you need to compute their gross hours per year.

Say your employee works 41 hours per week (= 8.2 hours per day x 5 days a week). By multiplying the number of their weekly gross hours by the average number of weeks in a year, you’ll get the related annual gross hours. Here’s the calculation:

41 hours per employee per week x 52 weeks per year = 2,132 gross hours per employee per year

Say this employee earns $30 per hour. To get your employee’s annual gross pay, multiply the number of annual gross hours by their hourly rate — see below:

2,132 gross hours per employee per year x hourly rate of $30 = $63,960 gross pay per employee per year

Step #2: Determine the net hours per employee per year

To calculate how many hours your employee actually works per year, you need to determine the number of hours they’re expected to be absent.

🎓 How Many Work Hours in a Year

Say your worker’s entitled to 10 vacation days per year. We’ll also say that they’ll be absent for an additional 5 days, due to illness and personal leave. That’s 15 absent days per year in total.

To compute their annual absent hours, multiply the number of their annual absent days by the number of daily gross hours. Here’s the calculation:

15 absent days per employee per year x 8.2 hours per day = 123 absent hours per employee per year

Now that you have your employee’s annual absence hours, you can calculate their net annual hours worked. Subtract the number of their annual absent hours from the number of gross hours per year, as shown below:

2,132 gross hours per employee per year - 123 absent hours per employee per year = 2,009 net hours per employee per year

🎓 Free 8-Hour Workday Calculator

Step #3: Calculate the total additional cost per employee per year

An employee’s labor costs are more than just their wages. They include taxes, benefits, and other employment-related expenses, so you’ll need to take those into account.

Say you pay $6,000 for payroll taxes, $5,000 for benefits, and $7,000 for other expenses per employee per year. That’s $18,000 in total for additional annual costs. The calculation goes like this:

$6,000 for payroll taxes per employee per year + $5,000 for benefits per employee per year + $7,000 for other expenses per employee per year = $18,000 total additional cost per employee per year

🎓 How to Keep Track of Expenses Accurately

Step #4: Calculate the total labor cost per employee per year

To compute your employee’s total annual labor cost, add up their gross annual pay and your total additional cost for that employee per year. Here’s the calculation:

$63,960 gross pay per employee per year + $18,000 total additional cost per employee per year = $81,960 total labor cost per employee per year

Step #5: Calculate the actual hourly labor cost

To find out how much labor costs per hour, divide your employee’s total annual labor cost by the total number of their net hours per year. This is the calculation:

$81,960 total labor cost per employee per year ÷ 2,009 net hours per employee per year = the actual hourly labor cost of $40.80

Step #6: Determine the labor cost percentage

Calculating the labor cost percentage helps you determine how much revenue is allocated to employee compensation. This allows you to assess your workforce efficiency and whether your staffing expenses are sustainable and aligned with your business goals.

To compute your labor cost percentage per employee, divide your employee’s total annual labor cost by your total revenue in a year (e.g., $1,000,000). Then multiply that number by 100. Here’s the calculation:

($81,960 total labor cost per employee per year ÷ total annual revenue of $1,000,000) x 100 = 0.082 x 100 = the labor cost percentage per employee of 8.20%

🎓 Productivity vs Efficiency: Maximizing Performance and Output

How to calculate the labor cost in construction

When it comes to construction projects, the best methods for calculating labor cost include:

- The unit pricing,

- The square foot, and

- The rule of two method.

Which method you’ll use depends on the project type, the required accuracy, and the available data.

Method #1: The unit pricing

The unit pricing method is typically used for project design or bid estimates. It involves calculating labor costs based on specific units of work or quantities (e.g., square feet or cubic yards).

Say a worker earns $25 per hour, and it takes 0.5 hours to install 1 square foot of roofing. This means that every square foot of roofing costs $12.50 in labor (= $25 x 0.5). If a project requires 800 square feet of roofing, the total labor cost will be $10,000 (= 800 x $12.50).

Method #2: The square foot

This method is often used for last-minute bidding. It calculates labor costs based on the total square footage of the project area. The square foot method assumes you already know a standard cost per square foot based on past projects.

🎓 The Ultimate Handbook to Construction Bidding (+ Steps and Tips)

In a flooring installation project, if the labor rate is $10 per square foot and the project area totals 2,000 square feet, the total labor cost will be $20,000 (= $10 x 2,000).

Method #3: The rule of two

Under this method, labor costs are assumed to be roughly equal to the cost of materials. While the rule of two method provides a quick way to estimate labor costs, it may not accurately account for site-specific factors and productivity variations.

If the project’s material cost is $5,000, the rule of two estimates the total project costs, including labor, at $10,000 (= $5,000 x 2).

How to reduce labor costs

Business owners should be proactive and seek ways to reduce labor costs. Here are several tips and tricks that will help you with that.

Tip #1: Use a time tracking system for employees

Tracking your employees’ time is a great way to boost their efficiency and productivity. Moreover, apart from motivating employees to be more productive on a personal level, it leaves less room for time theft.

According to time-and-attendance statistics, time theft costs US businesses at least $11 billion annually. So, ensuring your employees track time accurately can save you a lot of money.

Tip #2: Conduct regular time audits (preferably every month)

The process of investigating how time is allocated to specific tasks is called a time audit. It helps managers understand their employees’ daily routine.

By regularly comparing data for different projects or employees, it’ll become easier to spot where improvement is needed. Once you determine that, you can work on the necessary steps to increase productivity andidentify time wasters and inefficiencies.

🎓 25 Ways to Increase Productivity and Do More in Less Time

Tip #3: Invest in employees’ training

Companies that don’t invest in training are at a higher risk of their employees making mistakes. In fact, proper training equips employees with the knowledge and confidence to work independently, reducing the need for constant manager support.

By training your employees, you’ll not only improve their performance but also foster loyalty and reduce employee turnover.

Tip #4: Reevaluate employee perks

While benefits play a crucial role in employee retention, they’re often underutilized. That’s why you should ask your employees which benefits they actually value and use. This way, you can decide which benefits you can cut.

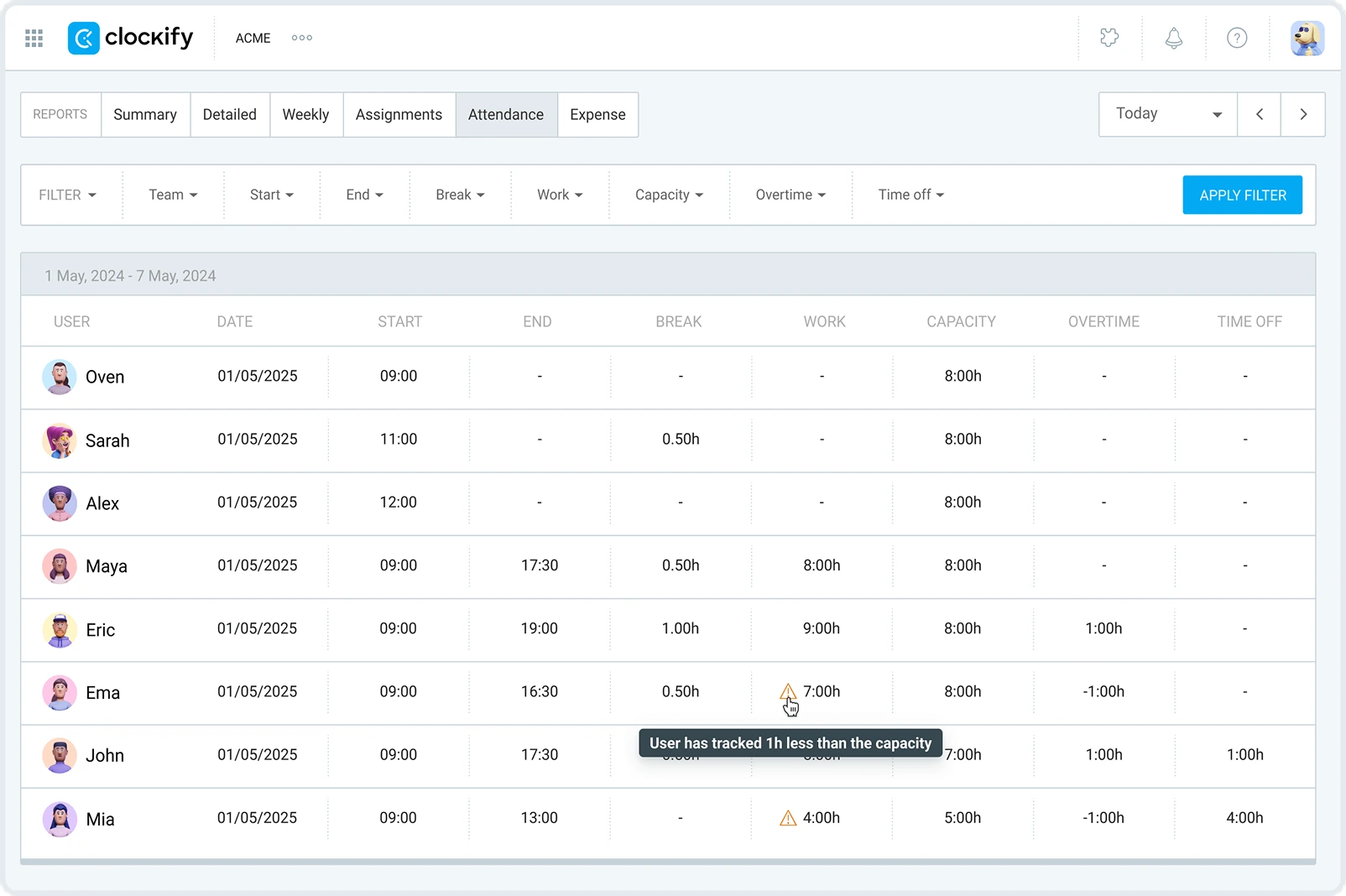

Tip #5: Keep overtime under control

In addition to tracking your employees’ regular hours, it’s important to track their overtime. This can help you reduce overtime expenses and prevent your employees from being overworked.

To track employee overtime, use a reliable time tracking tool like Clockify by CAKE.com. With this tool, you get to monitor your employees’ daily attendance, breaks, overtime, PTO, and capacity.

This allows you to optimize scheduling and maintain a healthy workforce.

FAQs about labor costs

Still have questions about labor costs? Then check out the following section.

What’s the formula for standard labor cost?

The standard cost of labor formula goes like this:

Standard hours (the time expected to complete a task or produce 1 unit) x Standard rate (the expected cost per hour of labor) = Standard labor cost

Suppose it takes 2 hours to produce a unit of the product. We’ll also assume the worker costs $15 per hour. Here’s how you’ll calculate the standard labor cost for this employee:

2 hours per unit x $15 per employee per hour = the standard labor cost per employee of $30

What are typical labor costs for a small business?

Typical labor costs for a small business include:

- Base wages/salaries,

- Payroll taxes,

- Employee benefits,

- Overtime pay,

- Workers’ compensation insurance,

- Training and development expenses, and

- Equipment and supplies (uniforms, computers, and other items employees need to do their job).

Most small businesses aim to keep labor costs within 30% of gross revenue to ensure profitability, though this varies by industry. Moreover, in the restaurant industry, costs can vary by service model (from 25% in quick service to 35–40% in fine dining).

How to calculate 7% off a price?

To calculate 7% off a price, you need to:

- Calculate the discount amount, and

- Subtract the discount from the original price.

To calculate the discount amount, multiply the original price (e.g., $80) by 0.07 (= 7 ÷ 100). Then, subtract that result from the original price to find the final (discounted) price. Here’s the calculation:

$80 x 0.07 = the discount amount of $5.60

$80 - $5.60 = the final price of $74.40

What’s the average cost of labor?

As the US Bureau of Labor reports, total employer compensation costs (wages and benefits) for private industry workers averaged $46.15 per hour worked in 2025. For state and local government workers, average compensation costs were higher — $65.68 per hour worked.

According to the National Restaurant Association’s research, labor costs reached a median of 36.5% of sales for full-service restaurants in 2024. Labor costs accounted for a lower median of 31.7% of sales for limited-service restaurants.

What’s an example of a labor cost?

It depends on the industry, but in healthcare, labor costs include wages, a night shift differential, and hospital nurse insurance.

What’s a labor burden rate?

The fully burdened labor rate is the total hourly cost of an employee. It takes into account not only their base salary but also all additional employment-related costs (otherwise known as “labor burden”).

Determining the fully burdened labor rate is crucial for operations directors as it reveals the true cost of employment (often 25–40% higher than base wages). This way, they can ensure every hour sold covers costs plus margin.

Which pricing model is right for my business?

The pricing model your business will use depends on your product or service, target market, and overall business strategy. Some of the most common pricing models are:

- Cost-plus (also known as “markup”),

- Value-based, and

- Flat-rate pricing.

Unlike value-based pricing (which focuses on the customer’s perceived worth of a product), cost-plus pricing relies on internal cost data. With cost-plus pricing, you determine a product’s selling price by adding a fixed percentage markup to the total production cost (materials and labor).

Many agency owners use this pricing method because it’s simple and ensures they cover all costs while earning a fair profit.

Flat-rate pricing is a model where a single, fixed fee is charged for a product or service, regardless of the time or resources required to deliver it.

What’s a contribution margin?

A contribution margin is a financial metric. It represents the revenue remaining from each sale after covering all variable costs associated with delivering that product or service.

The variable costs are expenses that change in proportion to production volume (they rise/fall as production increases/decreases).

What are the benefits of calculating labor costs?

The biggest benefits of calculating labor costs are:

- Improved pricing and profitability — it helps businesses understand the exact cost of labor, enabling them to set accurate prices for services or products. This way, they can maintain healthy profit margins.

- Accurate budgeting — it allows managers to ensure the project budget aligns with their team’s actual cost capabilities, reducing the risk of cost overruns.

- Optimized employee scheduling — it helps managers avoid over- or understaffing and adjust schedules to meet demand without unnecessary overtime expenses.

- Informed performance evaluation — comparing labor costs to revenue helps businesses evaluate operational performance and improve workforce productivity.

- Better client relationships — having clear labor-cost data enables managers to justify price increases to clients and build long-term trust.

Use Clockify by CAKE.com to track labor costs

Calculating labor costs helps business owners keep their business afloat and, eventually, profitable. However, manually combining everything to arrive at a single number is challenging, given the multitude of factors involved in the labor cost calculation.

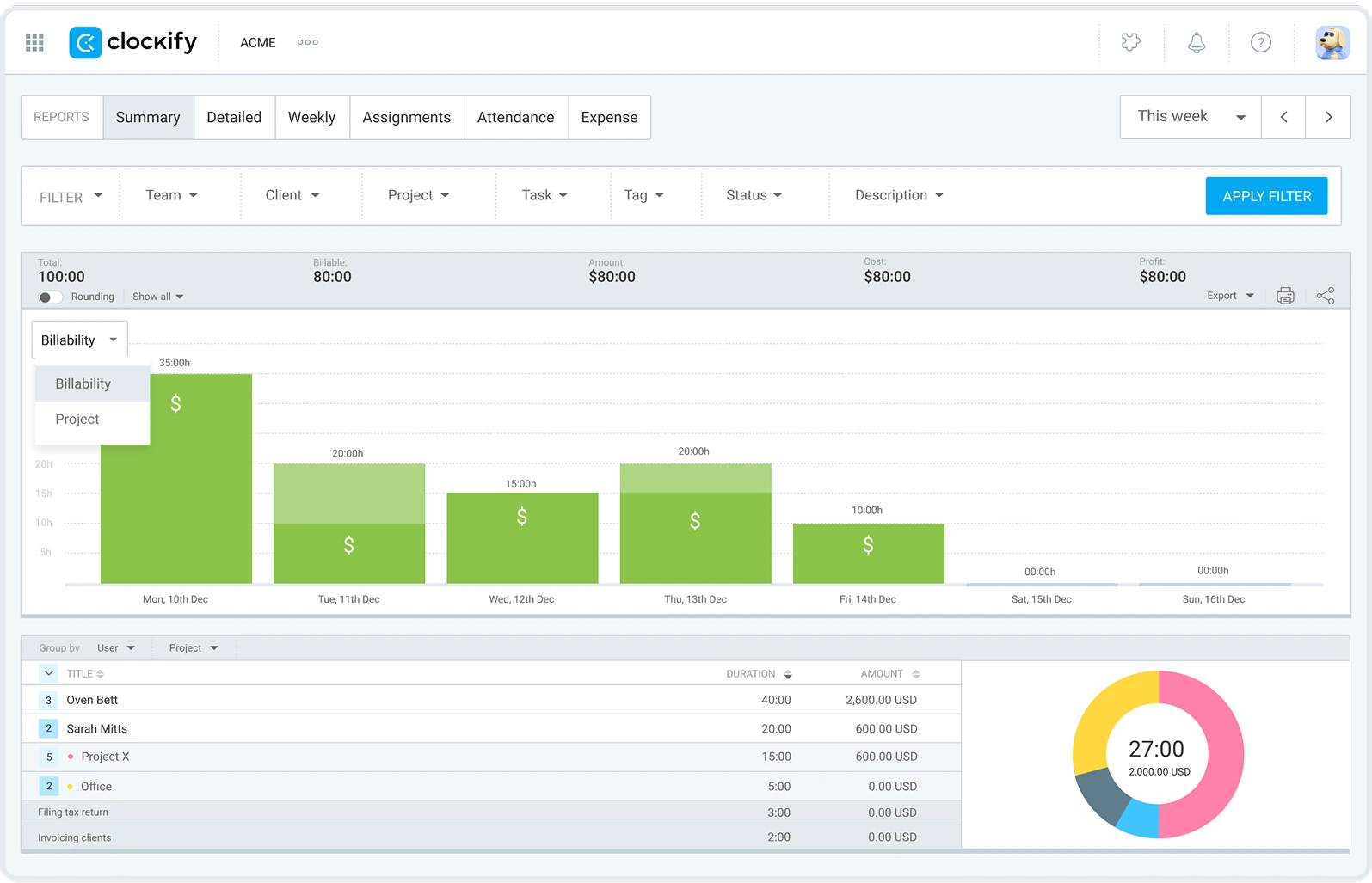

Therefore, the best thing you can do is track time spent on tasks and projects with Clockify to evaluate how your employees spend time at work. You can do that with Clockify Reports.

Clockify offers several types of time reports, including:

- Summary,

- Detailed, and

- Weekly report.

With Clockify’s Summary report, you can see the time spent on projects, billable and non-billable hours, and the total amount. Furthermore, you can filter reports by several criteria and export them in PDF, CSV, or Excel format.

Clockify by CAKE.com allows agency owners to:

- Track employee time with ease,

- Set up timesheet reminders for your team to maintain accurate records,

- Monitor project progress in real-time to prevent delays, and

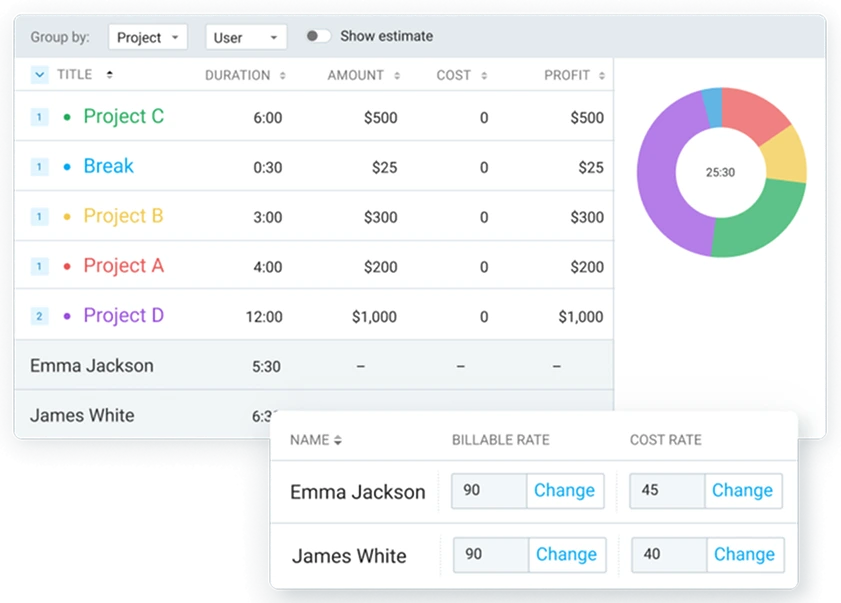

- Define hourly and cost rates to track and analyze project profitability.

This way, you can:

- Keep your employees productive,

- Identify and eliminate unprofitable services or clients, and

- Avoid undercharging.

Take control of your business and costs, make smarter decisions, and protect your margins — with Clockify.

To skyrocket productivity across your company, try a powerful CAKE.com Bundle. Alongside Clockify, you’ll get access to Pumble for business communication and Plaky for project management at a discounted price — $12.99 per seat/month (if billed annually).

Disclaimer: We hope this calculator/guide has been helpful. We strongly advise you to consult with relevant institutions or certified representatives before taking action on legal matters. Clockify is not responsible for any losses or risks incurred.