82% of project pros address issues before they even occur. They know that poor budgeting kills projects, leading to overspending and cutting corners.

But smart project cost management keeps revenue high and clients happy. To help you master it, we’ve cooked up a complete guide with:

- Clear explanations,

- Actionable steps, and

- Best practices (plus expert insights).

- Project cost management is the ongoing process of predicting, budgeting, and managing project costs.

- Strong project cost management leads to better resource planning, higher returns, and stricter cost monitoring.

- The main steps to project cost management are planning resources, estimating their costs, defining the budget, and controlling expenses.

- Managers use different cost estimation methods, such as reviewing past projects, analyzing measurable data, and consulting experts.

- Tailored apps like Clockify by CAKE.com help managers limit project spending through real-time and cost tracking.

What is project cost management?

Project cost management is the process of estimating, funding, and controlling expenses throughout a project. Managers apply it to create a baseline against which they can plan resources and the bottom line. Project cost management also helps you visualize a project’s financial status to avoid money leaks and cost overruns.

Beyond lower spending, the benefits of project cost management include:

- Better resource use — allocating the right amount of resources to different tasks during the project.

- Higher profitability — identifying cost risks and reductions with reliable data to increase revenue.

- Progress tracking — monitoring expenses to adapt quickly and uncover cost trends (critical for small businesses with strict budgets).

Seasoned project manager, Pavel Veselov, explains how to tackle internal and customer changes to limit spending:

“The manager should have a procedure for handling changes. We call this change management. The most important changes should be estimated for additional cost and time and approved by the project sponsor or committee.”

What is project costing?

Project costing is a small, specific process of forecasting and controlling spending for subtasks — NOT to be confused with project cost management, which is a big, ongoing procedure that covers the whole project.

When costing a project, you need to take several steps. If you’re implementing a security system for a client, you’ll:

- Size up their network setup,

- Split your work into phases (plan resources, install new software, and train the client to use the system),

- Look at immediate costs (license fees, total work hours, and training costs), and

- Define your project budget and emergency funds (for pesky incompatibility issues).

💡 CLOCKIFY PRO TIP

Want to calculate staff salaries and your operating overhead? Use this handy calculator:

Where does project cost estimation fit in?

Cost estimation in project management is the process of predicting the cost, quantity, and price of all the resources you need to deliver the project. It’s the starting point for both the project life cycle and project cost management.

Project cost estimation combines long- and short-term planning. First, you look at the overall project costs. Then, as you outline specific tasks, you identify detailed expenses to get them done.

In estimating costs, aim for:

- Precision — try not to over- or underestimate the cost of a project. Make an educated guess based on your goal, resources, and time frame.

- Accuracy — track time to get accurate work hours and simplify planning for future projects.

- Clarity — understand work requirements and limitations to avoid unpleasant surprises, like scope creep.

Key project cost management terms

So far, 2 terms keep popping up: project costs and project budget. Let’s clarify them.

What is a project budget?

Project budget is the total funds planned and allocated for a project within a limited time frame. It starts with an initial cost estimate and then depends on how well you track spending.

To better control costs, try these 4 main budget management types:

- Incremental — take your last project’s budget and add or subtract a percentage to create a new one.

- Activity-based — consider the number of activities around a project and decide how to price them to reach your target revenue.

- Value proposition — determine the value each project task brings to your business and allocate funds based on that.

- Zero-based — build your project budget from scratch and justify every activity before setting money aside for it.

What are the 5 types of project costs?

Project costs are the total expenses required to cover a project’s life cycle and they’re split into:

- Direct project costs that are directly related to a project’s completion, like providing custom market reports.

- Indirect project costs that aren’t immediately tied to projects (and can be fixed or variable). However, they’re necessary investments that keep the business running, like electricity bills.

- Sunk costs that you’ve already paid for and can’t recover. They can be direct or indirect costs, depending on whether they were attached to a specific project.

Knowing your total direct and indirect costs affects how you price services.

Here’s a cost comparison table with specific examples.

| Types of project costs | ||||

|---|---|---|---|---|

| Direct costs (costs of directly providing a service) | Indirect costs (costs that indirectly support project work) | Fixed costs (costs that don’t change during a project) | Variable costs (costs that fluctuate during the project) | Sunk costs (non-refundable costs that have been spent on a project) |

| Outsourced contractor fees | Regular employee salary | Server rent for the company’s website | Material prices (set by suppliers) | Declined project proposals |

| Computer equipment | Company-wide software licenses | Leasing office space | Revisions based on client feedback | Paid software for a specific project |

| Project/Case research | Staff training (workshops and certifications) | Insurance premiums | Traveling for client meetings | Research for a failed product |

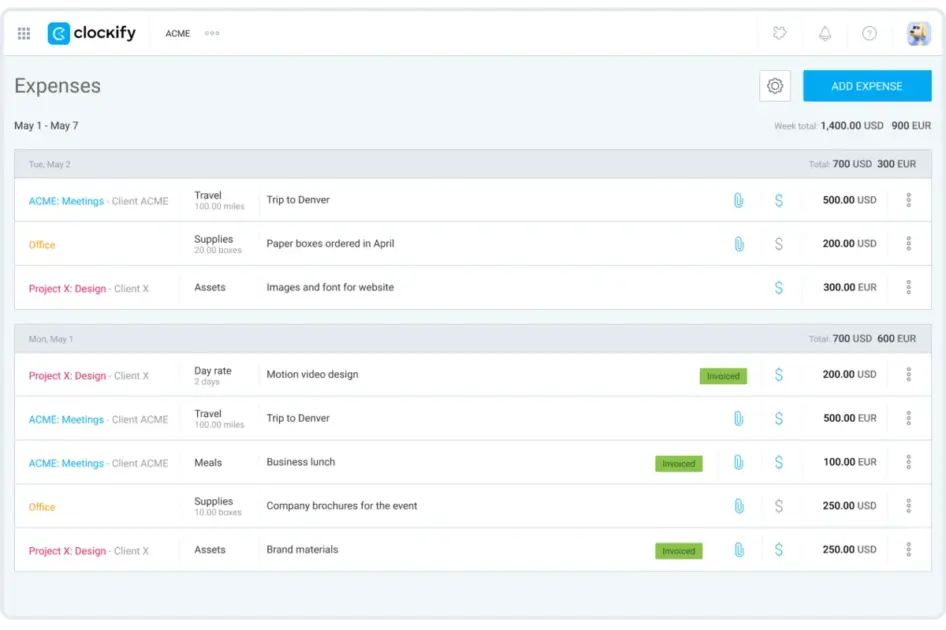

Track project costs in Clockify

What are contingency reserves and risk costs?

According to a study on project risk management, contingency reserves are extra cash you set aside to cover risk costs (or unexpected setbacks). Think major revisions or employee no-shows. So, having a contingency budget keeps risk costs from breaking your bank.

A contingency budget covers 5–15% of the project’s estimated funds. Say your project is valued at $400 — a contingency budget covering 5% of that would equal $20. Test it out with this formula:

Estimated project budget * (Contingency percentage / 100) = Contingency budget

How to manage project budgets

To stay on top of your budget (and cut costs where possible), you should:

- Train employees in efficiency — promote smart time tracking practices to improve your team’s performance and reduce project risks.

- Use new technology — introduce project cost-tracking tools like Clockify by CAKE.com to check spending in real time.

- Outsource tasks — hire freelancers or contractors to handle part of the work and lower costs.

- Cut overhead — review your expenses to spot cost-cutting opportunities, e.g., move to a smaller office or implement remote work.

How to calculate project management costs

Project management fees are a percentage of the total project costs and depend on the project scope, duration, and resources.

Say you set a PM fee at 7% for your $500 project. To get the PM costs, you’d multiply your total project expenses by 7%, which gives you $35. Try out the formula:

Total project costs * (Project management fee / 100) = Project management costs

Here’s how Wayne State University calculated project management (PM) fees for construction projects of all sizes:

| Total Project Cost (minus PM Fee) | Project Management Fee |

|---|---|

| $50,000–100,000 | 5.00% |

| $100,001–250,000 | 4.50% |

| $250,001–1,000,000 | 4.00% |

| $1,000,001–5,000,000 | 3.50% |

| $5,000,001–10,000,000 | 2.50% |

| $10,000,001–20,000,000 | 2.00% |

| $20,000,001 and higher | 1.50% |

As the table above shows, larger projects have lower PM fees. That’s because you can spread project costs across a longer timeline.

What are the 4 steps in project cost management?

To properly manage project costs, follow these 4 simple steps:

- Plan your resources,

- Estimate the costs,

- Determine the cost budget, and

- Control your costs.

#1: Plan your resources

Resource planning is the process of reviewing the project scope and identifying the necessary resources for project delivery. In particular, you should consider the type, amount, and quality of resources, which can include:

- People (employees, contractors, or freelancers),

- Team credentials and experience,

- Equipment (laptops and servers),

- Supplies (printing materials and SaaS tools) and

- Time allocated to each project task.

Track labor costs with Clockify

Then, create an effective resource plan that covers how many people you need, their skills, the equipment, and the exact project timeline.

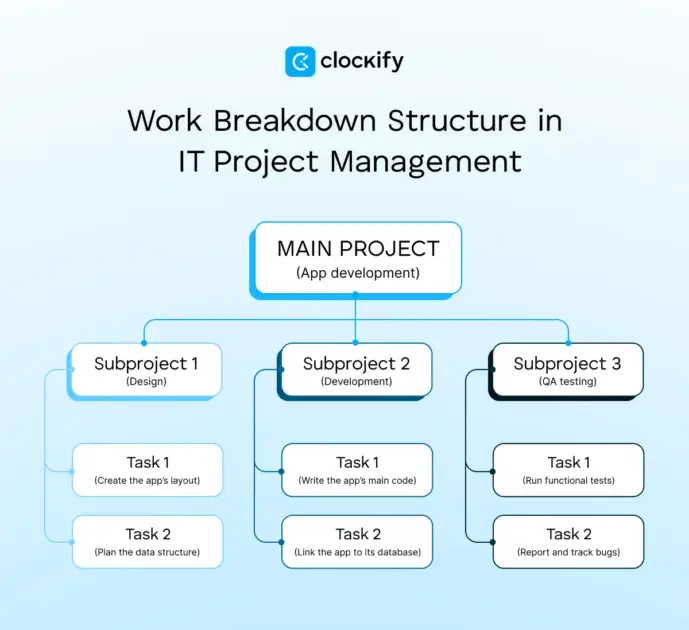

To kick off planning, most project managers use the Work Breakdown Structure (WBS). Forbes describes it as the process of breaking down large projects into smaller, manageable tasks. Visually, the WBS is a hierarchy with 3–5 levels, starting with the main goal and ending with tasks that lead to project completion.

After launching your project, use resource-tracking software like Clockify to get instant insights into time and costs.

SEO Manager, Derek Iwasiuk, plans projects proactively. He always assumes work takes longer than estimated:

“I allocate my time for friction before anything else. If a task is estimated at 100 hours, then I’m confident that it will be 120-130 hours after approval and revision come into play.”

Once you have a complete resource inventory, you can move on to the second step in project cost management.

#2: Estimate the cost of resources

Estimate the cost of project resources by reviewing the project scope and timeline to get the costs of labor, materials, and equipment. To ensure your project cost estimate is accurate, review past projects — compare their planned time and actual earnings. Get this data in time trackers like Clockify.

Besides software, check out some of the best project cost estimation methods in project management below.

| Project Cost Estimation Methods | Definition | When to Use |

| Analogous | Looks at general data from past projects (similar in size, complexity, and outcome) to gauge expenses for the new one. | In the early stages of project planning, and when historical data is limited |

| Parametric | Predicts the cost of a project by using measurable past data (like the labor rate per hour or cost per mile). | When you have tangible metrics and clear, repeating data |

| Bottom-Up | Estimates costs and time for each project-related task, and then sums them up to get the totals. | When projects have clearly defined tasks that you can assign time and costs to |

| 3-Point | Forecasts project length and expenses based on 3 average estimates: optimistic (O), most likely (M), and pessimistic (P). Applies the following formula:(O + 4M + P) / 6 | Best for risky, unpredictable projects, like upgrading old software or creating a market strategy |

| Expert Judgment | Determines project costs based on the knowledge and experience of seasoned estimators. | Best for projects with high uncertainty and scarce info |

#3: Determine the cost budget

You get the cost budget by summing up the costs of all project tasks and adding contingency reserves (extra money for unknown risks). This means aggregating all direct, indirect, fixed, and variable expenses. The cost budget helps you compare actual and planned costs for a project.

CMO at a software agency, Alys Reynders, breaks down her budgeting strategy. She looks at both “top-down project goals and bottom-up operational estimates to measure deliverables against a mock timeline.” Meanwhile, Alys stays prepared for changes by “using contingency reserves and real-time scenario planning.”

With a cost budgeting strategy, project managers can confidently predict costs for upcoming project stages.

#4: Control the costs

Controlling costs means tracking and documenting them all through the project. This process lets you react accordingly when things change, such as material or service prices.

To keep track of expenses, you should:

- Ensure the project stays within scope,

- Communicate with stakeholders,

- Follow the schedule and track your time, and

- Use project management software, like Plaky by CAKE.com.

On a deeper level, cost control is about tracking project progress against its cost baseline — the original, approved budget for spending during the project’s timeline. To make sure you stick to the baseline, keep tabs on 2 metrics:

- Cost variance shows you if you’re under or over budget, and

- Cost performance index tells you how efficient you actually are compared to the budget plan.

Managing director of an ad agency, Burkan Bur, shows what happens when you don’t control spending:

“A $40,000 job can lose 15% of its margins if not checked. Therefore, it’s safe to do weekly cost reviews against scope, time, and approved status.”

💡 CLOCKIFY PRO TIP

Learn how to track your spending faster with clear, custom budget reports:

How to monitor costs in real time

To nail project cost tracking in real time, explore different tactics. For example, try the Earned Value Management (EVM) method. It uses 3 elements to show if your project is on schedule and budget:

- Planned Value (PV) — cost of the work you plan to do by a certain date,

- Earned Value (EV) — cost of the work you’ve done so far, and

- Actual Cost (AC) — how much money you’ve actually spent.

With EVM, you can see how well you’re following the spending plan.

First, calculate the cost variance with the following formula:

EV – AC = CV

A positive CV means that you’re under budget and vice versa.

Then, get the cost performance index using this formula:

CPI = (EV / AC) * 100

You’ll get a percentage showing how much value you’ve created for the effort you’ve put in.

But what if you wanted to get warned about cost overruns before they happen? Then, you’d rely on a project cost accounting system. Clockify lets you predict when projects are about to blow your budget by showing:

- Completed time — total time tracked by your team so far,

- Forecasted time — expected delivery time based on already tracked hours,

- Scheduled time — amount of time you gave team members to complete their tasks, and

- Estimated time — your estimate of how long it would take to finish the project.

When the forecasted time starts to climb past the scheduled time, that’s your sign to make changes — and prevent cost overruns.

Track team time and project budgets — with Clockify by CAKE.com

Clockify can do 2 things at once — track time and monitor budgets. Apart from streamlined project cost management, our affordable time tracker offers 99.99% uptime and enterprise-grade security! In practice, this project cost accounting system lets you:

- Set hourly rates for people to track revenue and labor costs,

- Schedule projects or tasks and assign them to teammates,

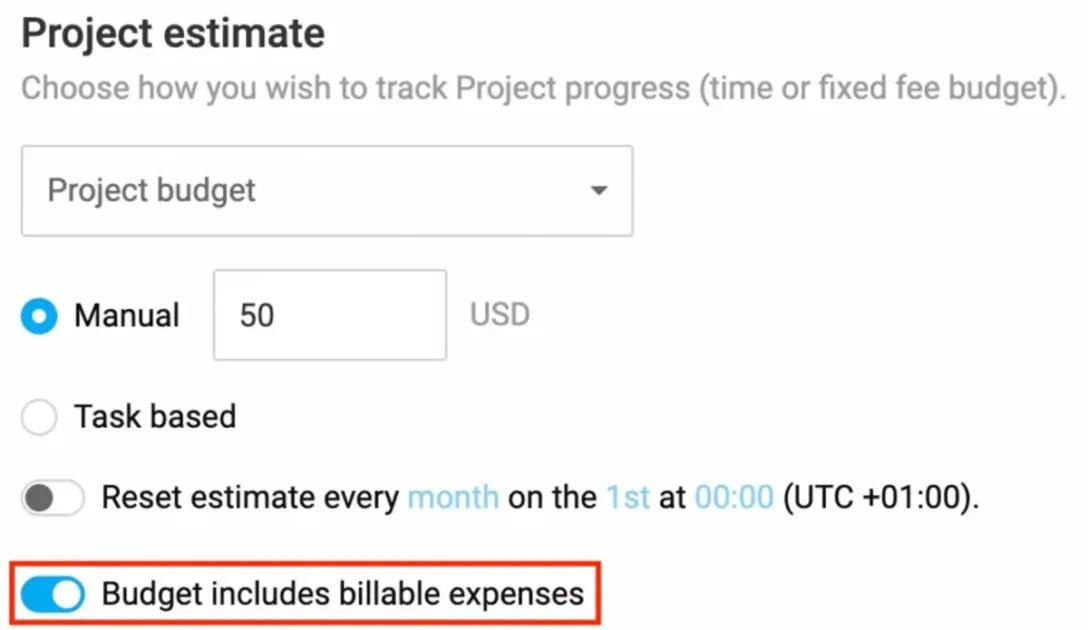

- Define and track budget or time estimates for projects,

- Track time with idle detection to spot inactivity, and

- Record project expenses by unit (20 miles) or sum ($15).

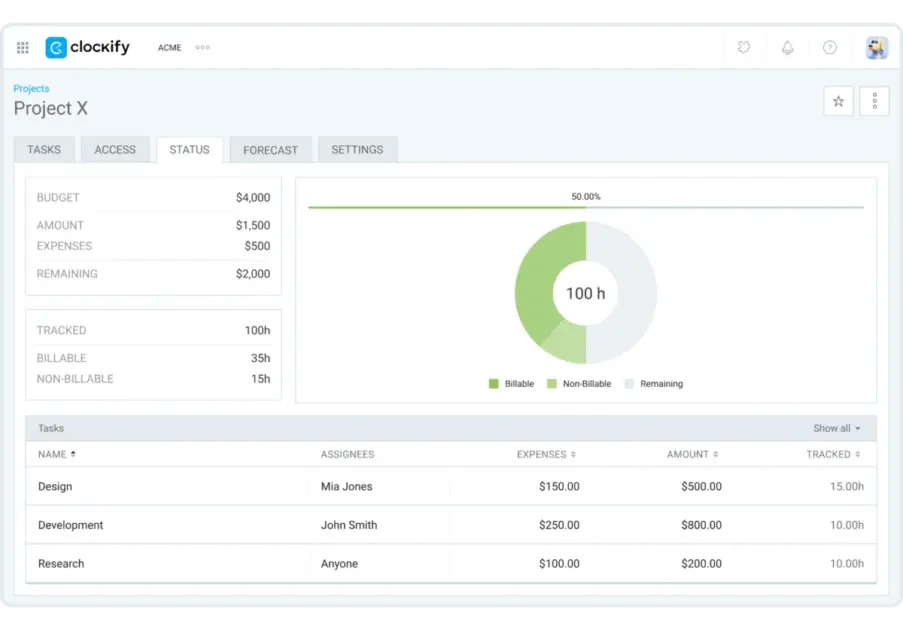

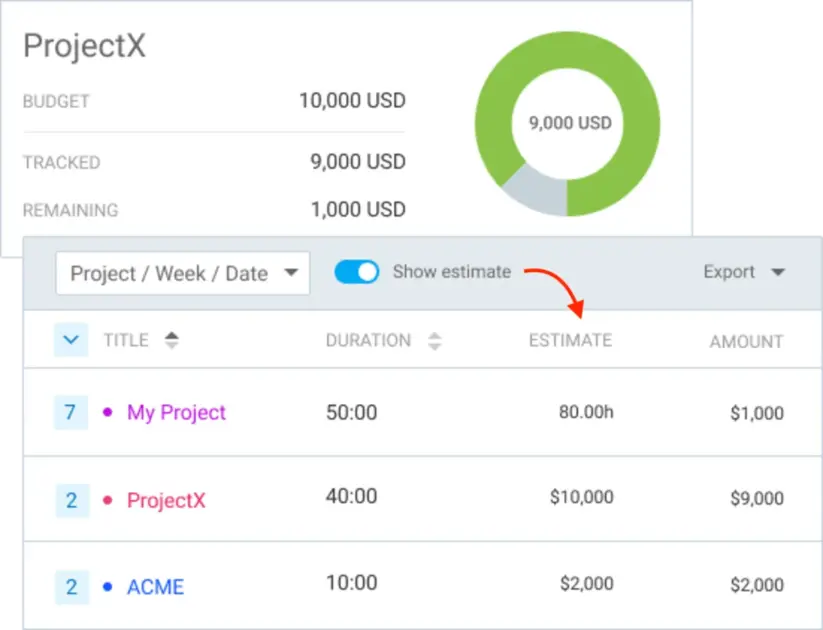

Additionally, Projects in Clockify come with 2 forecasting modes:

- Project status — see current tracked hours and profits against your estimates, and

- Project forecasting — predict future project outcomes, like how much it’ll take and cost.

To ensure your work matches your estimates, enable project Alerts. Clockify will send email notifications when your project hits a set percentage of the estimated time or cost. (Only workspace owners and admins can create Alerts.)

If your team’s work is repetitive, set your project as a template to get consistent, reliable results. This saves project-related tasks, billable rates, and estimates.

Clockify also offers smooth integrations to cover all aspects of project management. As part of the CAKE.com Bundle, Clockify pairs with:

- Plaky for visual project planning and status updates, and

- Pumble for dynamic team chats and video calls.

Looking for more goodies to power your project workflows? Visit the CAKE.com Marketplace for handy add-ons across categories such as IT & Project Management, Analytics & Reporting, and more.

Meanwhile, our 24/7 human support is ready to answer questions from both paid and free users. Plus, onboarded members get personalized guidance for free!

FAQs about project cost management

In this section, we demystify the most nagging questions about project cost management.

Do you need project management software?

You need project management software if you struggle to track projects, stay organized, and meet deadlines. Research backs this up. In fact, KPMG’s Global Construction Survey found that:

- 37% of firms miss project budgets and deadlines while

- 83% of firms have adopted, or are adopting, project management software.

It pays off by helping managers break down work and track goals with actual metrics. Clockify combines time tracking and project management to keep you organized without guesswork.

💡 CLOCKIFY PRO TIP

Torn between tools? Pick your favorite from this article, which lists top 3 project management apps:

What are the 4 types of cost estimates?

The 4 types of cost estimates include:

- Conceptual estimate — based on limited, preliminary project details,

- Detailed estimate — uses the confirmed project scope to list required materials, labor, and equipment costs,

- Quantity estimate — calculates the exact amount of supplies, workforce, and equipment, and

- Bid estimate — outlines the final price for the client, including overhead and profit.

As a project progresses, its cost estimate evolves from an initial rough approximation to a final precise figure.

What are the 7 types of costs?

Here are the 7 fundamental costs worth tracking:

- Rent or mortgage,

- Utilities,

- Payroll expenses,

- Cost of goods sold (direct production costs),

- Marketing and advertising,

- Insurance premiums (like property insurance), and

- Legal and accounting costs (for drafting contracts and bookkeeping).

💡 CLOCKIFY PRO TIP

Save money on accountant fees. Learn how to link Clockify with an invoice app:

What are the 5 basic cost concepts?

The 5 basic cost concepts in project cost management are:

- Standard costs — target costs set to cover supplies, labor, and admin expenses.

- Marginal costs — money you spend to intentionally expand the project by adding 1 more component, like a research report.

- Opportunity costs — profits of a project you pass up when choosing a different one.

- Differential costs — the difference in total cost between 2 decisions, such as picking between suppliers.

- Controllable costs — expenses that managers can influence during the project, like buying more printing materials.

What’s the difference between the cost baseline and cost budget?

The cost baseline is your approved spending plan, while the cost budget is your total planned capital + extra money for emergencies. In practice, the baseline maps out your project goals, which makes cost tracking easier. The budget defines your limits so that you don’t overspend.

What are the 4 principles of project cost management?

We’ve outlined the 4 principles of project cost management from research on managing project finances:

- Rely on accurate data to avoid underestimating project costs and overestimating the revenue.

- Track project progress consistently with a specific method (like a time tracker) to maintain transparent client reporting.

- Identify the expected project costs and benefits to ensure the project can sustain itself and turn a profit.

- Use cost-tracking tools to monitor how changes to your estimates affect the bottom line and to adjust quickly.

References

- Project Management Institute (2025). Pulse of the Profession® 2025 [Review of Pulse of the Profession® 2025]. In Project Management Institute (pp. 1–41). https://www.pmi.org/-/media/pmi/documents/public/pdf/learning/thought-leadership/pulse/pulse_of_the_profession_2025-1.pdf

- Ottaviani, F. M., De Marco, A., Rafele, C., & Castelblanco, G. (2024). Risk Perception-Based Project Contingency Management Framework. Systems, 12(3), 93. https://doi.org/10.3390/systems12030093

- Okeke, G. N., Obiorah, C. A., Ugah, T. A., Ali, S. E., Ukandu, O., Nesiama, O., Okoro, P. O., Babatope, C. O., & Akabueze, E. A. (2025). The Principles and Practices of Project Cost and Financial Management. International Journal of Innovative Finance and Economics Research, 13(4), 115–124. https://doi.org/10.5281/zenodo.17354053